Figure N° 1. Hypothesis and models for correlation

Source: Own Elaboration

______________________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________________________

Accounting demonstrations of political parties as an instrument for the effective transparency and accountability in the eligibility of electoral accounts

(*)Juedir Viana Teixeira; (**) Artur Angelo Ramos Lamenha; (***)Matheus Costa CorreaJoão; (****)Vinicius Santos Correia de Melo

(*) Candido Mendes University

Rio de Janeiro, Brazil

juedir@me.com

(**) Federal University of Alagoas

Maceió, Brazil

artur.lamenha@gmail.com

(***) Federal University of Alagoas

Maceió, Brazil

matheuscc1996@gmail.com

(****) Northeast University Teaching Society

Maceió, Brazil

jvscm93@hotmail.com

Reception Date: 11/16/2019 - Approval Date: 02/14/2020

DOI: https://doi.org/10.36995/j.visiondefuturo.2020.24.02.001.en

ABSTRACT

This article aims to present the importance of the accounting evidence in responsibility and transparency of the political parties’ accounts, especially in relation to the accountability of the use of the resources of the party fund. As a research question we have: Do accounts and candidates with irregular status and groups of political parties through the financial statements have a relationship with the distribution of the party fund and would require greater accountability? For this problem, it was established as a general objective to verify the need for the elaboration of more accurate and reliable accounting statements for the promotion of transparency, and as specific objectives, to discuss the legislation from the accounting point of view, as well as to understand the impact of the partial elaboration of the states with regard to the accounts judged as irregular and to groups of political parties according to the diffusion of their statements. For this, bibliographic, documentary and statistical research was used for the analysis and interpretation of the data extracted from the Court of Auditors, the Electoral Courts and the Legislation about this issue.

It is concluded that there is a positive correlation between the number of irregular accounts, the number of people with irregular accountability and political party groups with the distribution of the party fund and that the specific legislation about election accountability, as well as the rules of the Federal Accounting Council, can allow better transparency and social control with Accountability practices through the Accounting Statements.

KEYWORDS: Political Parties; Accountability; Financial Statements.

INTRODUCTION

Accounting Science provides useful and detailed information, as long as it is prepared in accordance with the opinions of accounting standards, so that the internal and external user of the organization, whether for profit or not, is fully aware of the financial, economic and patrimonial alterations. In this research, the aforementioned science will be addressed in the Third Sector, more specifically in political parties. In these nonprofit entities, accounting has peculiarities in regards to the technical part, however, in essence, it remains the same, that is, it must “capture, record, accumulate, summarize and interpret the phenomena that affect economic, financial and economic situations (Iudícibus et al., 2010, p.15). The particular technicality applied to political parties is anchored in the General Technical Interpretation - ITG - R1 - Non-profit entity. However, the legislation that disposes on political parties is not completely aligned with the opinions present at ITG 2002 - R1, which are particular and indispensable for the transparency of the accounts of such organizations. From the legal point of view, Act No. 9,096 / 1995, regulated by Resolution No. 23,546 / 2017, partially provides for the Accounting Statements, requiring only two, of a total of five, for sending to the Electoral Justice and its subsequent publication. Thus, the accountability or responsibility of political parties tends to lose quality, since they are not obliged to follow, entirely, the accounting rules set forth by the Federal Accounting Council - CFC and, consequently, decreases the opportunity to receive sanctions of the Electoral Justice. In accordance with Act N ° 9096/1995, those political parties considered insolvent against the Electoral Justice are not eligible to receive the Party Fund and, therefore, subject to sanction imposed by art. 37 - A of the Act that regulates them, that is, leading to the suspension of new accounts until the insolvency period elapses. Faced with the concern with the divergence of obligations and, consequently, the damage to the transparency of the information necessary for society, the following question is asked: Do accounts and candidates with irregular status and groups of political parties through the accounting statements have a relationship with the distribution of the party fund and would require greater accountability? Seeking to answer this question, it was established as a general objective: to verify the need to prepare more accurate and reliable accounting statements for the promotion of transparency, and as specific objectives: to discuss the legislation from an accounting point of view, as well as to understand the impact of the partial elaboration of the statements in regard to the accounts judged as irregular and political party groups according to the dissemination of their own accounting statements. This study is justified by discussing the role of accounting in the effective control of public expenditures, control policies of party funds and the improvement of accountability in political parties. From an academic point of view, it also serves to contribute with new studies in the area of control and audit of public and electoral accounts and stakeholder involved in electoral economic events. This work is divided into four chapters, where the introduction is in the first; a brief theoretical discussion about party legislation and accounting standards in the second; the methodology, presentation and analysis of the data in the third; and the final considerations in the last one.

DEVELOPMENT

Theoretical reference

According to Act No. 9,096, of September 19, 1995, which regulates and standardizes Political Parties, in its preliminary provisions objectively conceptualizes them and establishes in its art. 1st:

The political party, a private legal entity, is intended to ensure, in the interest of the democratic regime, the authenticity of the representative system and to defend the fundamental rights defined in the Federal Constitution (Act 9,096, 1995, art. 7).

They are social organizations formed by volunteers, legally authorized, with the objective of occupying political power. These organizations represent the people’s freedom of choice, which exercises democracy through voting and the legitimacy of elections. The political power, once reached, allows the parties to defend the interests and ideals of those citizens who placed their trust and want representation in the exercise of the mandate. The structure and organization of political parties are also defined by the aforementioned act, which establishes that parties registered in the Superior Electoral Court - TSE may be organized in the States and Municipalities through the establishment of definitive directories or provisional commissions, both regulated by the party statute.

According to the § 1º of the art. 7º of the Act in question:

Only the registration of the statute of the political party that has a national character is admitted, considering itself as such the one that proves the support of voters corresponding to, at least, half percent of the votes in the last general election for the Chamber of Deputies, without counting the blank and null votes, distributed by one third or more of the States, with a minimum of one tenth percent of the electorate that has voted in each of them. (Act 9,096, 1995, art. 7).

People’s sovereignty is exercised in elections for political positions through direct elections to elect their representatives, which contribute to the organization of public administration, maintenance of people’s rights and the execution of democracy; then, society has a very important role and mechanisms to control, participate, analyze and renew political people, their behaviors, legislation and organization of the State machine.

For this, it is essential that citizens know the structure of the parties, their financial sources, how they are organized, how they execute their operations, especially financial, and what their main obligations in relation to the competent bodies. Among the responsibilities of a political party, accountability is a differential in the democratic process, taking into account the need to make transparent the real situation of the party vis-à-vis society. In this way, those who are most committed to demonstrating information to the public tend to gain credibility in their promises.

Accountability is an act of exposing, through reports, reality and showing its mission to stakeholders. In the case of political parties, it is to have reliable information of the real administrative-financial situation for the entity to society and for the institutions and auditing bodies.

Milani Filho (2009) highlights the importance of the quality of the information transmitted, since it is not enough to just deliver the accountability on the date determined by law. The zeal in the realization of the reports is as important as the timeliness in their delivery. Prioritizing one feature over another only reinforces the idea of contempt for the user and for accountability.

These reports have a double character, as they attend to two different users with different requirements. The accountability report has a vertical and a horizontal approach. The vertical character of accountability is intimately related to elections and society's control over the actions of the rulers it elects. The horizontal character, on the other hand, refers to the state agents that supervise and punish other public agents, in this case, the Electoral Justice, when appreciating the leaders’ accounts and their respective politicians.

Vertical accountability refers to the representatives’ need to be accountable and submit to the population verdict, their epicenter being the election, which is the instrument through which constituents can control the activity of their representatives, being able to punish or reward them based on information related to their performance. (Pontes, 2008, p. 143).

Oliveira (2009) conceptualizes: "horizontal accountability corresponds to mechanisms of horizontal control between powers". According to O'Donnell (1998) it includes agencies:

Pontes (2008), when tackling the concept of horizontal accountability, perceives the function of Electoral Justice to mitigate the risk of omission or inaccuracy in accountability in order to contribute to the democratic process.The existence of state agencies that have the right and the legal power and that are, in fact, willing and able to carry out actions, ranging from routine supervision, legal sanctions to impeachment against the actions or emissions of other agents or agencies of the State that can be qualified as criminal. (O’Donnel, 1998 apud Pontes, 2008, p.40).

The participation of the Electoral Justice occupies the central position in the effectiveness of accountability, since it is through the supervision of political party activity and its publicity, with the availability of information from the decision-making process of accounts to the population that allows the control of society. (Pontes, 2008, p.143).

Both users of accountability, currently, enjoy a facility in the evaluation of reports due to technological evolution. Society and Electoral Justice gained quicker access to political party accountability, facilitating interaction with democratic institutions. Media, such as the Internet, facilitated transparency and developed faster interaction among information stakeholders.

Currently, it is used as a tool to present the accounting statements, the System of Accountability of Electoral Accounts - SRCE, foreseen in Resolution - TSE N°23.553/2017, according to the Manual of Operations of the SRCE - Registry, is a program developed by the Electoral Justice to help in the elaboration of the accountability of the candidates and political parties electoral campaigns. According to the resolution, accountability must be prepared through the SRCE, which must be installed in the user's computer to complete the information.

This tool, effectively, represented a great leap for Brazilian party politics in terms of accountability, taking into account the use of electronic media and leaving paper aside. However, Brazil's progress in this area is restricted to software, since the content, in general, transmitted via SRCE, continues without much credibility.

Melo (2017) conducted an investigation, in which he analyzed the political parties that elected representatives for the position of councilman in the 2016 elections in the municipality of Rondonópolis/MT, and also noted the fragility in the quality of the accounting information provided, as the parties barely achieve with legal requirements. As already mentioned in this study, there is a divergence between the requirements of the law and the accounting standards edited by the CFC, which generates an inevitable loss of transparency.

For the author, ´The political parties still develop an accounting in a very amateur way, only seeking through it to achieve with the current electoral legislation and do not use it in the best possible way´. (Melo, 2017).

Accounting and the professional accountant play an essential role in transparency and accountability through the presentation of acts and facts occurred in the activities with the purpose of satisfying the society that claims transparency and good faith in the use of public funds. In article 3, Resolution No. 23.546/2017 provides that the parties, in their accountability, must designate a qualified professional so that the technical qualification is passed to the procedures and becomes reliable.

Public funds are only one sort of income to guarantee the maintenance of political parties. These may generate cash in various other ways, since that the source of resource complies with the modalities established by section 5 of Resolution No. 23.546/2017. Any resource different from those listed in the abovementioned article is considered illegal or, at least, dubious and, therefore, must be thoroughly analyzed by the Electoral Justice.

With regard to the Special Fund for Financial Assistance to Political Parties, Party Fund, it is made up of budgetary allocations, electoral fines and penalties, legal financial resources and private spontaneous donations, according to Silva (1999). The composition of the endowment destined to the Party Fund is guided by Act N°9.096/1995, art. 38, point IV, in verbis:

Art. 38 The Special Fund for Financial Assistance to Political Parties – Party Fund- is constituted by:

[...]

IV – The Union's budget allocations, in a value never less than the number of voters registered until 31 December of the preceding year of the budget proposal, multiplied by thirty-five cents of real, at August 1995 values. (Act 9.096, 1995, art. 38).

In accordance with article 41 - A of Act No. 9.096/1995, of the total Party Fund, 5% - five percent - are allocated for delivery, in equal parts, to all parties that meet the constitutional requirements for access to these resources, and 95% - ninety-five percent - is distributed in proportion to the votes obtained in the last general election for the Chamber of Deputies. All those who do not violate art. 37 - A of Act No. 9.096/1995 are considered eligible to receive the Partisan Fund, which provides:

Art. 37 – A. The lack of accountability will imply the suspension of new quotas of the Party Fund as long as the insolvency persists and will subject those responsible to the penalties of the law. (Act 9.096, 1995, art. 37).

The deposits from the Party Fund must be made in bank accounts different from the other resources, according to Art. 6 of Resolution N°23.546/2017.

As regards expenses, according to Ferrari (2008, p. 86), "these are negative changes in net worth. Among other forms, they originate in the consumption of goods and the use of services. Their purpose, directly or indirectly, is to obtain income". The party expenses are established by art. 17 of the Resolution n°23.546/2017 in the following way:

All costs and expenses used by the organ of the political party for its maintenance and attainment of its objectives and programs constitute party expenses. (Resolution 23.546, 2017, art. 17).

In political parties, expenditures have a certain form of verification, in accordance with the provisions of Article 18 of Resolution No. 23.546/2017 as follows:

The verification of the expenses must be carried out by a suitable fiscal document, without amendments or erasures, the date of issue must be stated, the detailed description, the value of the operation and the identification of the issuer and the addressee or of the contracting parties by the name or company name, CPF or CNPJ and address. (Resolution 23.546, 2017, art. 18).

In this way, whenever expenditures of political parties were made, either by a natural or legal person, the supporting fiscal documentation must be provided, and there is also the limitation of electoral expenses, where penalties will be suffered in case of non-compliance with the provisions of Act No. 9,504/1997 as follows:

Art.18-B. Non-compliance with the expenditure limits set for each campaign shall result in the payment of a fine equal to 100% (one hundred percent) of the amount exceeding the limit without prejudice to the calculation of the occurrence of abuse of economic power (Act 9.504, 1997, art 18).

In accordance with article 32 of Act 9.096/1995, political parties are obliged to send, annually, to the Electoral Justice, the accounting balance for the fiscal year ended on April 30 of the following year. Chapter V of TS Resolution No. 23.546/2017 lays down some rules for party bodies, for example: use the digital accounting record.

Art.26. The digital accounting record comprises the digital version:

I – of the Daily Book and its auxiliaries; and

II – General Ledger and its auxiliaries;

1° The digital accounting registration shall comply with the provisions of this Resolution and the acts issued by Federal Treasury of Brazil and the Federal Accounting Council (Resolution 23.546, 2017, art 26).

This required evidence is important to provide results with maximum transparency, understanding and legality of the data collected. In Third Sector entities, specifically political parties, it is valid to understand the financial and economic situation of organizations that use and manage public resources, that is, resources of the entire society that properly pays their taxes and does not want to see unnecessary or illegal waste.

In order to improve the transparency of political parties, it would be interesting to demand a more detailed accounting, more efficient control bodies, better quality reports and the strengthening of existing laws, since accounting and accountability are preventive measures and control tools to combat the lack of clarity in policy. The operability of party accounts is the enemy of the development of a healthy political environment and can affect credibility, party affiliations and third-party donations, reaching revenues and hindering their maintenance.

The idea that accounting science is only important to for-profit entities is rather outdated. This applied social science is not only obligatory, given a legal imposition, but it is a necessary management tool that helps managers and users in decision-making and, in the case of political parties, also promotes transparency for the owners of the resources that these entities manage: society in general.

Given the referential presented, the relations between persons, accounts and political parties considered irregular are investigated from the point of view of the analysis of the transparency of party funds, as well as the relation of the groups of parties that present a set of accounting statements in relation to the others.

Methodology, presentation and data analysis

This work, according to its objective, was classified as an explanatory research because its main concern was to identify the factors that determine or contribute to the occurrence of a certain phenomenon (Gil, 1991). In accordance with Lakatos and Marconi (2011), explanatory research records facts, analyzes them, interprets them and identifies their causes. The purpose of this practice is to broaden generalizations, define broader laws, structure and define theoretical models, relate hypotheses to a more unitary vision of the universe or productive sphere in general, and generate hypotheses or ideas through the force of logical deduction.

It is also necessary to use bibliographic research. According to Gil (1991), bibliographic research is carried out on the basis of material that has already been produced, consisting mainly of scientific books and articles. Documentary, bibliographic and statistical analysis was used to carry out this work, with the help of two software SPSS, PAST and EXCEL-XLSAT, with the following hypotheses and models:

H1: There is a correlation between the values transferred by the TSE and the number of irregular accounts in the statements;

H2: There is a correlation between the values transferred by the TSE and the number of people with irregular accounts in the statements;

H3: There is a relationship between groups of political parties that present a greater number of accounting statements with the transfer of party funds to those groups.

Figure N° 1. Hypothesis and models for correlation

Source: Own Elaboration

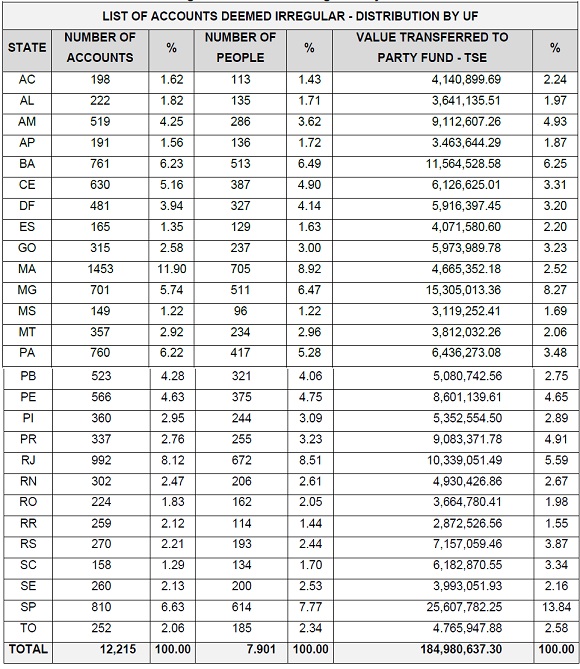

Next, the situation of irregular accounts was analyzed observing all federal units, considering as variables the number of irregular accounts, the number of people with accounts judged irregular and the value transferred to the party fund, according to the data of the TSE and TCU, in concert with Table 1:

Table N° 1. Irregular accounts according to TSE y TCU information

Source: Own Elaboration on the basis of TSE and TCU data (2018)

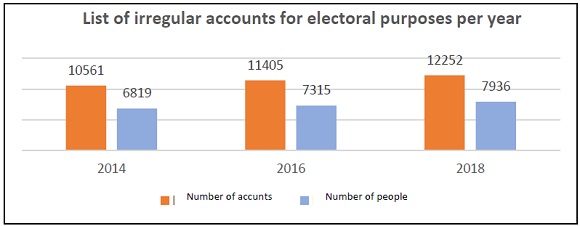

Consulting the TSE database, there is an increase in the number of irregular accounts that must be observed in relation to the problems revealed in the referential of this work. An evolution is perceived according to the graph presented below.

Graph N° 1. Evolution of irregular accounts for electoral purposes

Source: Own Elaboration on the basis of TSE data (2018)

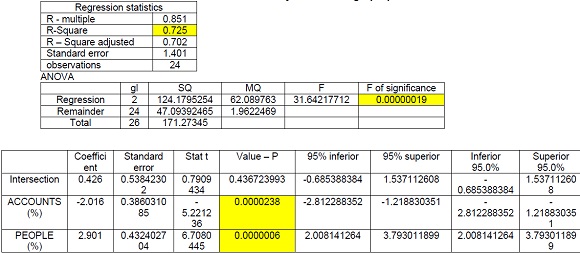

After the presentation of the table, statistical tests were carried out to verify the determination coefficient and the p-value by the regression between the variables and for the treatment of the data, the statistical analysis, the construction of tables and graphs the EXCEL software was used with the XLSAT supplement, according to what is demonstrated below:

Table N ° 2. Statistical analysis of counting x people

Source: Own Elaboration

As set out above, it is verified that 72.50% of the variables number of accounts and people with irregular accounts are explained by the variable transfer from the TSE to each state, as well as the test shows the coefficient f of significance of 0.00000019 and by the low values of p of the variables of 0.05. Next, We then proceeded with the correlation between the variables, seeking to verify hypotheses H1 and H2:

H1: There is a correlation between the values transferred by the TSE and the number of irregular accounts in the statements;

H2: There is a correlation between the values transferred by the TSE and the number of people with irregular accounts in the statements:

Correlation matrix (Pearson):

Table N ° 3. Correlation matrix (Pearson)

Source: Own Elaboration

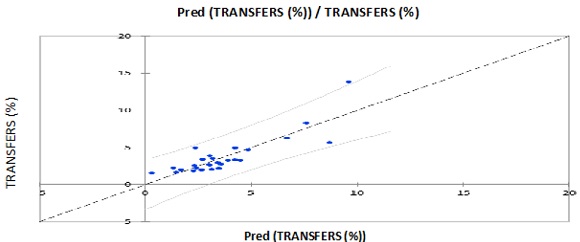

After the statistical analysis it is possible to present the model below:

TRANSF.TSE = 0.425862112148234 -2.0155593516345*CONTIR +2.90057658135448*PESCONTIRREG

The graph below shows a good distribution of data and remainder, with a good adjustment of the straight line to the set of data, as they tend to fluctuate to both sides without necessarily following a model of behavior, which confirms H1 and H2.

Graph N° 2. Distribution of coefficients and analysis of transfer residues

Source: Own Elaboration on the basis of TSE data (2018)

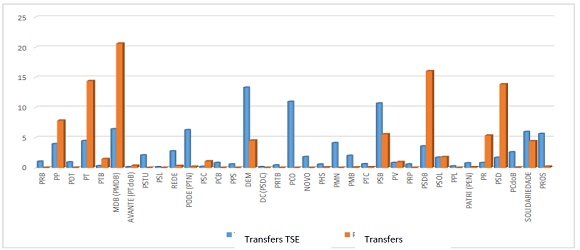

The distribution of transfers from the party fund to all political parties is shown below, in accordance with the legislation, as well as the transfer of the values transferred to the regional directories, even with parties that do not transfer any value to their regional directory, this reinforces the need for effective accounting for values received and expenditures, as well as patrimonial variation between coalitions and between national and regional directories to identify possible inaccuracies with legislation and, consequently, reduce the number of irregular accounts.

Graph N° 3. Transfers from the Party Fund to parties and from parties to directories

Source: Own Elaboration on the basis of TSE data (2018)

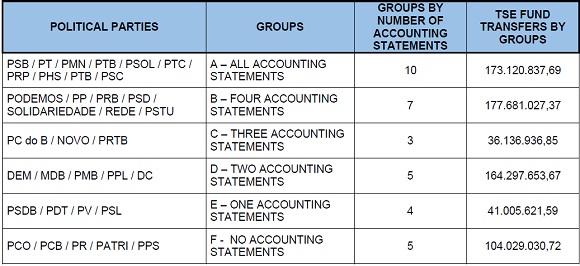

Based on the data collected on transfers to political parties, information was collected on the websites of the political parties and the TSE on the accounting statements, classified by group of parties that had similarities in the amount of accounting documentation submitted, according to the table below:

Table N° 4. Distribution by group of parties x number of accounting statements

Source: Own Elaboration on the basis of TSE and parties data (2018)

In order to analyze these data, based on the reference of this study, hypothesis H3 was formulated: There is a relationship between the groups of political parties that present a greater number of accounting statements with the transfers of party funds to the referred groups.

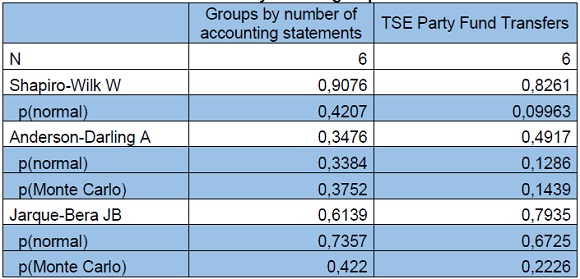

To apply the appropriate statistics to present the model and to demonstrate the hypothesis, we proceeded with the test of normality and from the results, we opted for parametric tests:

Table N° 5. Normality test for groups x transfers

Source: Own Elaboration using PAST

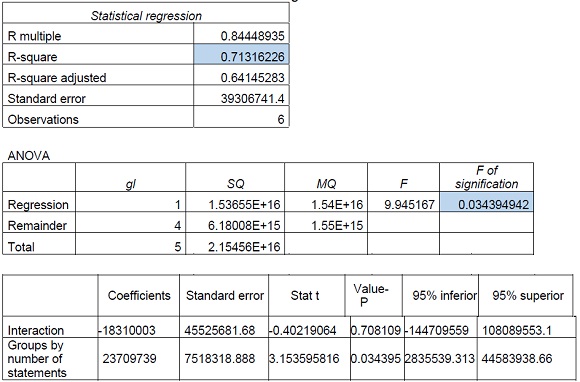

The report with the results of the ANOVA statistical analysis is presented below, highlighting the values of R2 of 0.713 and p of 0.034.

Table N ° 6. Regression statistics

Source: Own Elaboration

TSE Fund Transfer = -18310002.9464634+23709738.9873171*Groups by number of accounting statements

In this way, H3 can be confirmed: There is a relationship between the groups of political parties that present a greater number of accounting statements and the transfers of party funds to these groups, since it is interpreted that, given R2, 71.32% of the variability of the transfer of funds by the TSE, which is the independent variable calculated in the ANOVA table, and given the level of significance of 5%, that is, 0.034, the information provided by the explanatory variables was significantly better than a basic average, as observed in the graph below:

Graph N° 4. Regression of Party Fund Transfers x Group

Source: Own Elaboration based on research data (2018)

Considering all that has been exposed in this investigation, it is verified the need of an effective control in the transfer of resources, with the purpose to obtaining more information in the accountability of the political parties that follow to the letter the requirement of Act nº 9.096/95, regulated by Resolution Nº 23.546/2017, regarding the presentation of Accounting Statements before the Electoral Justice.

“Art. 4º Political parties, at all levels of leadership, must:

[..]

V - to refer to the Electoral Justice, within the periods established in this resolution:

The Federal Accounting Council - CFC, in turn, through the ITG 2002 - R1 establishes specific criteria and procedures regarding the elaboration of the Accounting Statements for the third sector entities, where the political parties fit in, and includes three more pieces not addressed by Resolution Nº 23.546/2017.

Knowing the competence of the CFC to address and regulate accounting and its professionals, it is understood that the survey of these three pieces omitted by the legislation brings more transparency to the events occurring within the parties and, consequently, propitiates the Electoral Justice to prevent cases of corruption in the country.

CONCLUSION

Accounting, as a management aid tool and main source of information for users, should be used more by audit bodies, especially Electoral Justice, taking into account the possibility of combating and preventing corruption through a thorough analysis of all the accounting statements referred to in the ITG 2002 (R1).

For the accountability of political parties, a minimum of information is required, mentioning only two accounting statements established by current legislation, the accounting-financial situation throughout the calendar year.

The present investigation demonstrated, quantitatively, the fragility of party accounts, taking into account the growth of 16% of those considered irregular, in an order of magnitude of tens of thousands of accounts, between 2014 and 2018. This abnormality is strongly influenced by the disparity between the current legislation, as far as party finances and accounting are concerned, and the accounting regulations, edited by a body with a wide domain in this field of knowledge: Federal Accounting Council.

In this way, the general objective of the study presented is considered to have been achieved, i.e., to verify the need for the preparation of accounting statements for the promotion of transparency, since the two pieces required by Resolution No. 23.546/2017 must be complemented with two other pieces established in the ITG 2002 - R1/.

In line with the above considerations, the existence of a moderate positive correlation between the values transferred by the TSE and the number of irregular accounts in the statements is now highlighted in technical terms, as is a substantial positive correlation between the values transferred by the TSE and the number of persons with irregular accounts in the statements.

In this sense, there is a perceived need to use an accounting practice that is fully in line with the standards and instructions of the CFC. This autarchy, with all its organization and expertise in the field, could dialogue with the Electoral Justice and join efforts to prevent and combat the low quality in the exercise of accountability, ensuring the regularity of party accounts and promoting the expansion of an environment free of fraud and focused on satisfying the needs of society. The great advance in the political party field would be an audit in the moulds of the securities market, except for the due proportions. In other words, the CFC would act freely as the Securities Commission - CVM, pressuring the parties to observe good accounting practices and facilitate public access to financial information in addition to making the actions of the Electoral Justice with regard to the protection of public resources more pleasant.

Also, the importance of the role of accounting in the transfer of resources from the TSE party fund to the parties and from these to their regional directories can also be observed, since it is possible to note the concentration of these resources on the part of some parties, and others that they transfer without the qualified information of these events, which also does not allow for follow-up by the justice system and control bodies, such as the courts of accounts and public ministries.

According to the specific objective of understanding the impact of the partial preparation of the accounting statements with regard to accounts judged to be irregular and the transfer of resources via party fund, it is also considered to have been achieved during the investigation, considering the finding of a correlation between the values transferred by the TSE and the number of irregular accounts in the statements; a correlation between the values transferred by the TSE and the number of people with irregular accounts in the statements; and, also, a relation between the groups of political parties that present a greater number of accounting statements with the transfers of party funds to those groups.

This research was limited, through a qualitative and quantitative approach, to the confrontation between the diffusion of the Accounting Statements, determined by law, which, in fact, establishes obligations and sanctions for non-compliance with the rules and the diffusion determined by the technical-normative text of the accounting area, which has an instructive and enlightening bias. In this way, it is verified that the existing gap between the two norms, legal and technical, allows the execution of accountability of dubious accounts and of difficult inspection by the Electoral Justice, taking into account the absence of sanctions and continuity in the transfer of resources of those parties with few presented accounting statements. Nevertheless, for future investigations, deeper and more representative studies of the accounting-financial situation of the political parties are stimulated, individually, directed towards the criteria of evidence proposed by the accounting regulations.

BIBLIOGRAPHCIAL ABSTRACT

Please refer to articles Spanish Biographical abstract.

REFERENCES

Please refer to articles in Spanish Bibliography.