Financial Planning of Agricultural and livestock compañies

Sanchez, Carlos Omar

“Visión de Futuro” Año 13, Volumen Nº 20, Nº 1, Enero - Junio 2016

URL de la Revista: http://revistacientifica.fce.unam.edu.ar/

URL del Documento: http://revistacientifica.fce.unam.edu.ar/index.php?option=com_content&view=article&id=409&Itemid=88

ISSN 1668 – 8708 – Versión en Línea

ISSN 1669 – 7634 – Versión Impresa

E-mail: revistacientifica@fce.unam.edu.ar

________________________________________________________________________________

Financial Planning of agricultural and livestock companies

Sánchez Carlos Omar

Facultad de Ciencias Económicas y Jurídicas

Universidad Nacional de La Pampa

Santa Rosa, La Pampa, Argentina,

estusanch@yahoo.com.ar

Reception Date: 31/08/2015 – Aprpoval Date: 18/12/2015

ABSTRACT

In this piece of paper an analysis of the handling of funds in the agricultural and livestock is approached, verifying some theoretical issues but –most fundamentally- putting emphasis on practical aspects. Owing to this fact, the financial planning as a tool of administration is associated with the productive, economic and investment plan, showing to be efficient in the currency resources. The financial planning is substantial in the agricultural and livestock companies, as much as there is an extended period of time because of the expenditure of consumable goods or services and the originated incomes in the products sale.

This study alludes to an analytical and empirical approach as well, to keep up with the demands, considering not only theoretical aspects, but also issues regarding the praxis on account of the interview results made to different actors of the area and the author’s experience as producer and assessor of agricultural and livestock companies. By means of such application moments of new investments can be examined in accordance of the relative prices, which could derive on an analysis of the convenience, without borrowing loans, acknowledgement of the influence (positive or negative) of an inflation process and the gaining of a realistic and straightforward praxis.

All in all, a model of the cash flow is presented, which farmers and stockbreeders producers can carry out, on account of the dynamic and flexible function recognition of such plan, considering updating quarterly.

KEYWORDS: Financial planning; Relative prices; Cash Flow.

INTRODUCTION

The head of an agricultural enterprise must have knowledge and expertise in two key areas. In the production area and in the area of administration.

It is commonly found in rural areas to producers with extensive knowledge, both theoretical and practical, on the specific activity carried out in the estate or property; however there is the same availability of knowledge regarding rural administration or management of agricultural enterprises, according to the Anglo-Saxon or French respectively doctrine is followed.

Those who believe the administration or management as the axis on which should turn the other functions in any organization, including those engaged in agricultural activity, we recognize it as vast and complex as engaging and non-delegable task. In this sense, the management is "... the set of knowledge and techniques of production and economic nature, which allow the use and optimal implementation in the short and long term, of available inputs are endogenous or exogenous to exploitation" (Management livestock enterprise, 2010).

At the same time, we know that means organizing manage, provide, coordinate, monitor and evaluate. These tasks are carried out by a process that requires accurate, timely and useful information; however the rural environment is characterized by information often incomplete and sometimes random, such as weather and price variations (for both the sale of products, as for the acquisition of inputs).

The administration, despite everything, is the most important to conduct an agricultural enterprise tool and basically includes the planning and decision-making and planning precisely aims to eliminate or at least reduce uncertainty; which improves the ability of decision of the employer.

We know that planning can be classified as:

a) Time: short, medium and long plans.

b) Amplitude: partial or global plans.

c) Flexibility: flexible or rigid plans.

In this paper we particularly deal with a partial planning, as is the financial plan and the flexibility of this tool of the administration or management, with a practical approach.

There is no doubt about the need to plan for any type of business with different time horizons, which is extended to organizations engaged in agricultural activity. Partial or complete plans form the basis of a modern administration, in order to avoid improvisation, predict well in advance, adjust production to available resources, planned with control executed to determine the causes of failures, etc.

The statement allows us to infer that proper planning in farming, must include a production plan, an economic plan, an investment plan and a financial plan. So we try to demonstrate the importance of the latter and its link with other management tools.

In agricultural enterprises need financial planning, it emerges from the characteristics of these companies; since many of them have incomes once or twice a year and expenditure, with varying intensity, it occurs every month. At the same time in many activities that make expenditures costs happen with great anticipation, for resources generated by sales according to production cycles.

To cover this deficit we propose the following objectives: describe financial planning, recognize some difficulties in its implementation, verify how to carry it out, simply show the annual-active funding and presenting linking financial planning with other plans the company.

DEVELOPMENT

1.- Finance and administration

Currently the use of money reached such importance that the vitality of a business or company depends primarily on the generation of resources and the use made of them; so much so that disciplines that study minutely obtaining income and expenses arise.

The allocation of funds carried out effectively, is the foundation for achieving the benefits that are expected to obtain and ensure the growth of the company; for this reason it can be said that "... finance is the art and science of managing money, so that financial management is a discipline that helps us to plan, produce, control and direct our economic life" (Visa: Finance practices, 2005).

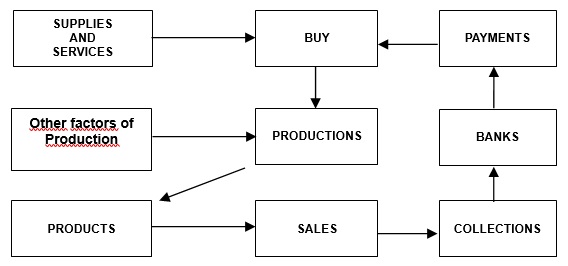

In farming, like any other economic activity, the circuit of money resulting from the basic operations: applying inputs to produce, obtain products, place them on the market, collection of sales, as a means of ensuring availability for paym

In the elementary circuit aceste flow line, it can be seen in the following scheme:

Figure N° 1: Basic Operations

Source: Own Elaboration based on E. Martinez Ferrario

In these basic operations should be very carefully, so that the flow of money circulation is not impeded and proceeds reach the form and at the right time to meet their commitments. Therefore, handling money comprising:

The finance manager must therefore manage (usually scarce) monetary resources to obtain funds in the most convenient way and apply or allocate them in the most efficient manner. But money management is not an isolated event in the business life where there is concurrence of multiple factors that determine the actions to take, as in the case of fluctuations in market prices (where the producer is not forming price, but taker them), levels of inflation rates and lending rates, technological advances, the exchange rate, the tax burden, etc.

Companies are in an exposed to changes in an almost permanent basis and requires them survival means some degree of flexibility to adapt to them. These changes should not be made in a context of uncertainty and improvisation; therefore, a realistic and flexible financial planning so as to eliminate the threats and seize the opportunities offered required.

2.- Financial planning

In accordance with the above we are able to assert the need for such planning, with the highest degree of accuracy possible, to make it a useful tool for the management of agricultural enterprises.

Perform planning with the highest degree of accuracy possible not mean it's foolproof, because the implementation of activities show the reality, but this should not detract from or discredit this administration tool that aims to:

Solve liquidity problems in advance.

-

They are prepared to take more effective and efficient decisions.

-

Economically exploit the excess funds circumstantial.

-

Cover the shortfall in funds at the lowest possible cost.

-

Show the components of the company the cost of money and its impact on the results in each sector of it.

-

Perform a general and critical assessment of the liquidity conditions in which the organization will unfold.

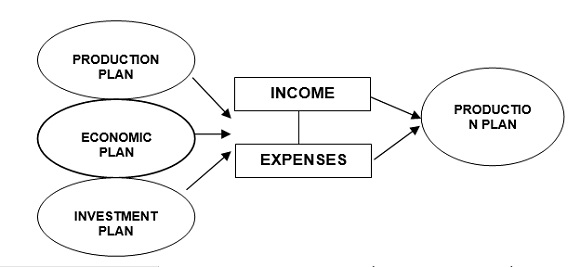

The preparation of a financial plan is the result of comprehensive planning of agricultural enterprises; since it is necessary to have a production plan, an economic plan and investment plan.

While it is true that, for interviews, most companies do not have written plans mentioned; many have an approximation of them mentally; therefore, know what will be the activities to develop in the next production cycle and the intensity of them, as well as based on the estimated results are considering investments such as renovation of machinery, new infrastructure work, etc. Therefore, it is part of elements and too generic information and, often disjointed that hinder the realization of a more or less solid financial plan and adjusted to the future of the organization.

Then we insist on the need for productive, economic planning and investment to develop a degree of approximation a financial plan, whose main feature will be to take into account the time of inflow and outflow of funds, because it should work about the perceived and not on accrual. Put another way interested in knowing when the sales are charged as inputs acquired or contracted services are paid.

Financial planning, based on productive, economic and investment plans can be graphed as follows:

Figure Nº 2: Basis of financial planning

Source: Prepared on the personal experience of the author

The intersection or interlocking circles, representing production plans, economic and investment shows the close link between them, so they should behave synchronously; at the same time they provide information of income and expenditure provided for the preparation of the financial plan through a cash flow or cash flow.

2.1 Difficulties in developing a financial plan

There is no doubt that improvisation, sooner rather than later, generates unnecessary or superfluous costs far more so if it comes to the finances of a company where the funding is intended to cause interest and, in case of default, accrue to punitive damages and other expenses that could be avoided.

Given this reality we must prepare a financial planning to allow control of monetary resources to effectively manage agricultural enterprises on an item of administration we have observed-for interviews with producers themselves the greatest deficiency, since it is common to find with two prototypes of producers:

The ultraconservative not make investments until they have enough money to meet them, which wasted relative prices or the leverage effect, as appropriate; or they are punished for inflationary processes that make you lose purchasing power.

-

Those who bet so exaggerated borrowing, thinking that macroeconomic circumstances in the country will allow them to pay debts without shock. While it is true that at times it is possible, is not a constant; since the change in relative prices of commodities versus cost, causing misalignments that punish mercilessly recurrence of this way of managing resources.

The difficulties to overcome are:

Having a consistent, realistic and detailed production establishment plan, considering the working surface, supplies, personnel, estimated production, dates of work, harvest or harvest, sales, billing and payments.

-

Develop an economic plan to calculate the results of the activity, according to previous planning, based on probable realizable value and cost.

-

Prepare a plan of possible investments into two groups: those of essential character and desirable but could be delayed in time; considering the possible funding of these structures.

-

Changes in relative prices compared to agricultural production, which modifies the working scenario of producers in a substantial way and involves being very alert and flexible to make decisions very quickly or 'march' plans.

-

Unpredictable weather contingencies that alter production plans and even prices, which demands an immediate adaptation to new circumstances.

-

Inflationary processes that modify the values of sales and costs evenly sometimes and sometimes in different degrees or percentages (relative price changes). Many times there are changes in input prices gradually and almost constant, while output prices are changed 'by steps or jumps', after many months of stability.

The aspects mentioned in the previous items are the basic elements to develop a coherent and realistic financial plan; however, the quasi-permanent changes to what is under the agricultural enterprise by internal or external to the same issues, requires a flexible preparation and therefore subject to frequent changes.

Consequently, the financial plan is a dynamic tool, to respond quickly to quantitative and qualitative changes of production, price changes of the products obtained and the necessary inputs, climatic alterations are these favorable or unfavorable, modifications in the macroeconomic environment in general, etc.

2.2 How to prepare a financial plan

As an initial part in developing a financial plan should consider three important issues namely:

a) Take into account the difference between accrual and perceived. The first as the recognition of a right or the generation of an obligation and the second as actually received by that law or actually paid by that obligation.

This perceived difference between accrued and is fundamental to everything related to financial issues. For clarity, it is exactly the same as that between a bird flying and a bird in the hand. Moreover, in strictly financial terms that phrase translates as; earned a bird and a perceived bird. (Mondino, D. E. and E. PANDAS, 1997, p. 35).

Mindful of the statement is vital for business management, consider the time period for the collection of sales and payment terms obtained for purchases and which we will return later

b) Recognize the existence of inflation, "a phenomenon that never meant a general rise in prices as they trumpeted many authors for decades ..." (Pungitore, JL, 2003, p. 53) whose price changes translate into a change in relative prices clear and unquestionable; and "... during inflation a transformation occurs in the relative prices of different goods. Some prices rise more than the average and others less "(Ferrucci, 1986, mentioned in Pungitore, J. L. 2003, p. 53).

For the purpose of making financial planning, in relation to inflation, often make two mistakes:

Assume that does not exist, and

-

Assume that the increase will be generalized and, therefore, its effect will be neutral.

Therefore appropriate precautions should be taken to carry out this task, the same as making the necessary adjustments when macroeconomic issues require.

c) Finally, as a result of the above in paragraph b) it should be considered holding results; since the lack of neutrality of inflation is compounded by exposure to inflation of certain assets and liabilities, which can cause positive or negative effects on finances. For example it is sufficient to cite accounts receivable and payable.

The first, according to the term of perception, it is a negative effect and considering the payment terms (no interest), the second a positive effect will be obtained; the same applies to stocks of inventories.

We having clarity on the above, we are able to begin the task of financial planning. This forces us to determine the income and expenses, measured in pesos, for a period of time given.

Such a procedure can be performed if previously, agriculture, cultivation has been determined to intensify or diminish their production, that, based on the available-surface (it is a limited resource in the short term) allows us to set the area in hectares to be allocated to each type of crop (whether for harvest or as fodder resource).

With the previous data we are able to determine the tools to use, work, man hours of work, the necessary inputs (fuel, seeds, agrochemicals, etc.) and consequently the probable and normal production.

With regard to livestock activity if we must differentiate breeding, wintering or full cycle. Broadly planning tasks should start with initial stocks of cattle by categories, destinations and status of them.

The first classification is to separate the assets (wombs and males) of inventories (heifers, steers, heifers, calves / as and cows refugo). Then knowing the state can know if they are coming to sell or yet to wean or weight achieved adequate animal slaughter.

With these initial data can be inferred sales, purchases for replenishment, consumption of green forage or grain henificado, health costs and veterinary care, expenses for marketing, etc.

2.3 The long-term financing

Financial planning horizon, need production forecasts and likely sales value and costs, can not extend beyond three to five years by the big gap that may occur. Despite this it is necessary in the agricultural sector and particularly in the livestock because production cycles are longer than in agriculture, particularly in cattle breeding.

At the same time obtaining long-term loans (3 to 5 years) it requires us to analyze the ability to repay such loans and efficient way to perform this analysis is through the development of financial planning with a time horizon as mentioned.

Surely this planning adjustments that may be required semiannual or flat rate, based on the facts or circumstances occurred, should be shortened to a quarter or extend this period up to one year.

There is no doubt that this planning allows:

a) Avoid jolts temporary underfunding derived from circumstantial and unexpected illiquidity.

b) To find the best rates due advance funding, allowing the reduction of operating costs.

c) Foresee enough sales to meet its commitments time, avoiding hasty marketing reduces bargaining power.

d) Attempt to 'fit' income and expenses, in an attempt to not have idle availabilities facing a deteriorating purchasing power of the currency.

e) Ensure the leverage or leverage credits applied to activities whose rate of return exceeds the effective rate of the loan.

f) Emphasize achieve a favorable result tenure through transfer credits and take debts, which often provides the economic situation.

We are convinced that the farmer can not be oblivious, for efficient administration, this way of management that achieves frankly favorable results.

Finally against recurrent inflationary processes showing the economy of our country, with the aforementioned consequences of the change in relative prices, it is particularly useful to efficiently manage the agricultural enterprise, have annotations or registrations to product value. This is useful to know how many kilograms of wheat, soy or bullock were necessary and are currently required to sell for a watered-down, buy a planter or pick up.

This comparison allows investments, improvements or renovations when the least amount of product obtained in establishing needed. In other words, the unit of account for the agricultural entrepreneur is not the weight, or a foreign currency (eg dollar) but the good it generates.

The product obtained allows him to discern when something is 'expensive or cheap' in relative terms or value-product; You can even purchase inputs for the next season or production cycle, when the value- product cost is lower.

2.4 - year-asset Financing

The short-term financial planning can cover a production cycle or have one year horizon, which does not necessarily coincide with the calendar year; because we are convinced that this vital management tool should have two main characteristics:

a) Be flexible. This means the possibility of correction, adjustment and adaptation with relative ease and frequency, so as to allow follow in the footsteps of climate variations (with delay or advancement of work), levels of production (for exceeding or not reach original goals ), the changes in absolute prices and relative (for rise or fall that were ignored at the beginning of planning) and, therefore, by the postponement or advances in investment plans that were originally aspired.

b) Maintain the planning horizon. For it is also necessary to adjust and update, add at least quarterly a period equal to again have a plan for the next twelve months.

For consultations conducted we know that 98% of livestock producers operate with official or private banks; the same total 95% have a checking account (where you pay or extract money by issuing checks) and almost 40% operate with more than one bank.

This brings operational convenience, in most cases, customers of banks are authorized (within certain limits) to deliver or overdraw. Just the higher rate of interest of financial institutions, is the current account overdraft. Of consultations many respondents agree that often hold negative balances (overdrafts) in current accounts and that it is taking for funding agility and comfort, not having planned ahead of the funding they need.

On the other hand,

from a financial point of view, it should have a low sum credit (accounts receivable) and a significant amount of debt (accounts payable) that do not accrue interest, which creates leverage that benefits the company with the use of foreign capital. (Sanchez, C. O., 2010, p. 104)

Finally, to achieve consistency with this plan we call year-active flow of funds in accordance with the production planning should be done by checking the biological cycles, moments of harvest or harvest eventualities markets and timing of cash receipts and payments usual. In this regard it should be noted that it is preferable to take five to seven days to the expiration of collection, due to delays in transfers, check cashing, etc. as a safety margin to avoid transient desfinanciamientos.

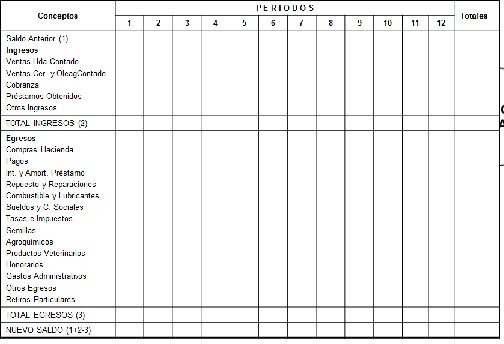

Then we add a tentative formula or template, to prepare a cash flow annually in agricultural enterprises.

Figure Nº3: Cash Flow Worksheet

Source: Prepared on the personal experience of the author

As the flow of funds is prepared for monthly periods is important to note that within the same month, there may be a payment on day 2 and a charge on the 30th and this can lead us to think that we are funded and actually have a phase shift of 28 days. This case can be solved including payment in the previous month or the month after charging to achieve consistency and show the reality as it is. Overall charges must precede payments in about five days.

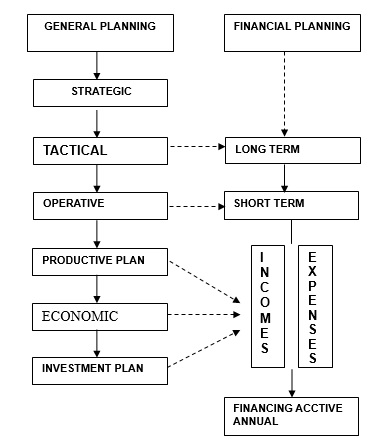

To summarize a diagram showing the relationship between the general planning and financial planning at various stages it included.

Figure Nº 4: Summary of Financial Planning

Source: Own calculations based on the Administrative Process

2.5.- Practical way to develop the Flow of Funds

Based on what was stated in the preceding paragraphs, we are able to prepare, in greater detail the income and expenses so we try first the resources. The money supply can come from:

1 (I) - Sales of products

2 (I) - Collection

3 (I) - Sale of fixed assets

4 (I) - Credits obtained

5 (I) - Capital contributions

1 (I) - Determination of sales are made based on the estimated considering, in an optimistic, pessimistic or more likely criterion, the latter crop or livestock production. The calculated physical products are multiplied by the market price, which usually operates producer, based on the above criteria taking chances.

However it is convenient to subtract between 5 and 10% on the figures calculated as a safety margin, in response to unfavorable weather contingencies or unexpected price drop.

At certain values there must be deducted selling expenses, which can be estimated at a percentage of the sales amount, in order that if adjustments need to be made only be modified income.

Finally note that cash sales will be taken and that, if sales shall be recorded according to the date of recovery.

2 (I) - The collection to include term sales are not received in the previous section, as sales are recorded as perceived.

3 (I) - Sales of assets if it is true that are not regular, should be considered in financial planning in order to have control over the resources and expenditures. Often these revenues are related to the investment plan for renewal of machinery and tools.

4 (I) - Credits earned are generally made loans in financial institutions, credit or bank, which may be short or long term according to their destination.

Income must be received by or credited into account and should be foreseen in the loan amortization expenses and interest, according to payment dates or cancellation net worth.

5 (I) - This includes any capital contributions or additions that make the producer or the members of the organization.

Regarding expenditures should be analyzed, based on production planning, each considering the physical volume of costs or expenses and estimate currency, also based on the most likely values as the date of disbursement. Generically and, depending on your treatment, we can group the outputs of money without prejudice to later- greater detail in the following items:

1E) - Direct costs or variables

2E) - Fixed costs or structure

3 (E) - Obligations with suppliers

4 (E) - Bank loans

5 (E) - Purchases of goods exchange

6 (E) - Investments

7 (E) - Private Retreats

1 (E) - Direct costs arise plan mixed agricultural production, livestock or and includes expenditures on personnel, fuel and lubricants, seeds, agrochemicals (fertilizers, herbicides and pesticides), needlework third (spraying, harvesting, chopping or haymaking, etc.) among others.

2 (E) - Fixed costs, also called indirect unable to seize irrefutably to the production of a good, are considered based on the payment date and includes: property tax, maintenance of infrastructure work, expenses management, electricity, mobile telephony, etc.

3 (E) - payments to suppliers In those outstanding obligations are taken in the previous year, because purchases and expenses of this period are recorded at the time of payment.

4 (E) - Partial or total cancellation of bank loans should be considered based on their respective maturities expenses, commissions and interest.

5 (E) - Purchases of inventories in the livestock business, are important wintering activity and should be taken into account when payment for the replacement of animals.

6 (E) - Outputs investment by purchase or renovation of machinery for construction work improvements or new facilities (gouaches, fences, etc.) shall be recorded according to the dates of payment thereof, is at cash or installments.

7 (E) - Particular withdrawals to meet the needs of the owner and his family or partners within the company, must be taken into account in order to have total control over the finances of the organization.

We must not forget that the increase in spending on families (for their growth, children who continue to higher education, for the acquisition of new technologies, etc.) generates growing needs of funds and this results, especially when it is the only resource or livelihood in funding needs of enterprises. Some achieve it by intensifying their production, others being more austere or deferring investments; but others end up compromising their survival by failing to consider these expenditures as logical, as necessary.

With detailed financial planning elements that we believe, consistent with the overall planning, a very useful tool for the management of agricultural activity is made; but it must be flexible and, therefore, should be updated at least quarterly to consider the positive or negative variations in production and prices

Considering as described above, are able to affirm that the less seasoned without significant training, farmers are able to manually or by other means developing the Flow of Funds (Figure No. 3) return; whose quarterly update allows to carry out active annual planning (section 2.4).

Such a claim is to have implemented a group of producers who developed it, just give some basic and elementary instructions, which strengthens our insistence on its implementation.

2.6.- Funding Sources

Complementing financial planning we want to add a synthesis of the various sources of funding, noting advantages and disadvantages they offer and that-conocerse- help lower costs.

To that end we must distinguish that the capital has all agricultural enterprise, is fixed capital (buildings, improvements, machinery, tools, etc.) and working capital or working capital (livestock, inputs, cash, accounts receivable, etc. .) in both cases they can be supported or financed by own or third party resources.

Third party resources may have different origins, such as suppliers, bank loans, overdrafts, credit cards and leasing, as explained below:

a) Try: Funding obtained from suppliers is common in all economic activity. Normally suppliers often provide credit to their customers, in the case of agricultural enterprises does not exceed 30 to 60 days for almost all inputs, except fuel to shorter lead times (between 7 and 14 days).

In any financing, interest where no pattern, there is usually an interest or implied financial burden that is included in the price or value of the products. Therefore, the farmer what to look at first is the price difference between the operating cash and payment term, in order to determine the rate charged for attempting such funding. Then the implicit rate should be compared with actual inflation rate, in order to determine whether to accept or not the funding provided by the supplier or if it is more convenient to take a bank loan.

b) Bank loans: Signing a bank credit requires a detailed analysis in order to determine whether to take it. In general we must agree that contracts to take a bank loan, are contracts of adhesion, ie, there are no possibilities to discuss certain clauses. In other words, it is the creditor imposes conditions and the debtor can only be the possibility of accepting or not.

Known conditions: with or without collateral (personal or real), term, interest rate and other expenses, the main analysis should be the destination of the loan, the possibility of return (repayment capacity) interest rate compared to the likely rate of inflation and improvement in income that can generate the loan.

While it is true that it is often convenient to change debts with suppliers or short-term, long-term bank loans or, it is important to analyze whether what the company needs is capital rather than a credit.

c) Overdrafts: The ability to deliver without proper funding or failure of these checks, it is an alternative discouraged by the high interest rate charged by banks, however in specific and temporary situations can be used in amounts which are not significant in the operations of the company in question.

d) Credit cards: Banking institutions often have specific credit cards for the agricultural sector, such as: Agro Nation (Banco Nacion Argentina), Galicia Rural (Banco Galicia), Caldén (Banco de La Pampa), etc. with excellent plans between 180 and 360 days for payment, which allow financing at a very reasonable cost, and that all livestock producers should consider.

e) Leasing: The rent to own, offering many banks can be a very interesting way to renew machines, tools or pick ups within the farm. Monthly fees are costs that allow computing the VAT as a tax credit and no ownership of the asset, so the Personal Property tax is not paid.

Accordingly, this alternative may be useful for companies engaged in agricultural activity and deserves to be analyzed rigorously in each particular case.

CONCLUSION

Financial planning is another element within the overall planning and development process is linked to the operating face of the company therefore has an indissoluble and vital link with the praxis.

Management, management, day to day, acquires an unobserved by many producers, a management tool that will yield positive results as fast as instrument relevance. No such specific or outstanding training is necessary and all producers can put it into practice through an Excel program or simply handwritten sheets with columns and rows suggested.

What more emphasis should be, and there may need more training, is inflationary processes in the evaluation and management of relative prices and in use, parallel to the flow of funds manner, the unit of account value -Product for making important decisions, allowing it to generate quantitative and qualitative leaps of importance in the company.

By having each employer its assets exposed to inflation, aware that it is not neutral and that it are winners and losers, consider getting results for positive holding that under certain circumstances or contexts, substantially alter the future of the organization.

We are nevertheless convinced that many farmers, having endured inflationary processes of different intensities and at different times, have acquired certain skills in financial management against loss of purchasing power of our currency.

We must also highlight the need to adapt often the financial plan, compared with price changes and climate variations, to constitute a useful tool in the administrative process in order to make better decisions that help to achieve the goals envisaged.

Our view is that this work, although abbreviated treatment, can become, for those less familiar with the principles of administration, on the axis on which turn any attempt to efficient management.

We conclude the same confidence that you have reached our initial proposal, since we show the real operation and the ideal; at the same time provide a simple working model with minimal training.

The practical aspects developed in paragraphs 2.2, 2.4 and 2.5 are clear evidence that the practice is achieved easily and constitutes an axis about which can rotate the administration, from a group encounter with very basic and elementary explanations. In short its implementation does not depend on the level of training, but the conviction of its usefulness and, of course, the will to carry it out.

BIOGRAPHICAL ABSTRACT

Please refer to articles Spanish Biographical abstract.

REFERENCES

Please refer to articles in Spanish Bibliography.