Internal control proposal for municipalities based on the survey and analysis of second category municipalities in the province of Misiones

(*)Ana María Czubarski; (**)Letizia Mariel Paprocki; (***)Alejandra María Lorena Ramírez; (****)Mariana Villamayor Nercolini

(*)FCE - UNaM

Posadas, Misiones, Argentina

anaczubarski@gmail.com

(**)FCE - UNaM

Posadas, Misiones, Argentina

letiziapaprocki@gmail.com

(***)FCE - UNaM

Posadas, Misiones, Argentina

aml-ramirez@hotmail.com

(****)FCE - UNaM

Posadas, Misiones, Argentina

marianavillamayornercolini@gmail.com

Reception date: 10/04/2022 – Approval date: 12/02/2022

DOI: https://doi.org/10.36995/j.visiondefuturo.2023.27.02.002.en

ABSTRACT

Currently, municipalities are in a stage of institutional strengthening addressing different tools to improve their management. Although they advance in different topics, in general they focus on aspects of legality control aimed to comply the required rendering of accounts.

A good internal control implementation would contribute to an improvement in management, presenting benefits both for these organizations and for the citizenship.

This article intends to address the current situation of internal control in small municipalities, from the survey and analysis of the second category municipalities of the province of Misiones, Argentina, in order to know through quiz of municipal accountants, what activities are carried out in this area and carry out an analysis of different aspects that could be improved in the light of good practices of this type of control.

These municipalities are taken as the unit of analysis since, being small and having a reduced administrative structure, they allow us to know the reality of the small municipalities of the country, the conclusions being applicable to the latter.

KEY WORDS: Internal control; Municipalities; Management.

INTRODUCTIÓN

The internal control is of great relevance in the organizations in the search of the optimization of the operation of the administration. It implies a tool for the implementation of a proactive action, in order to significantly reduce the multitude of risks to which the different types of organizations have been exposed.

Control in general is essential in any type of organization, and especially in public entities, where they constitute a pillar of the democratic system and a guarantee for citizens of the use of public funds.

Internal control is exclusively addressed in this article, in general terms, that is, referring in its broadest sense to management control, since by law in the municipalities of Argentina, it is not usually included in the legal framework of this type of entities An external and internal control is foreseen and indeed carried out, but strictly referring to technical legality controls.

Public entities need to have the highest possible degree of reasonable security regarding the efficient and effective use of public funds, allowing the fulfillment of their functions. For this reason, added to the controls that are effectively carried out in compliance with legal regulations (external and internal, technical and legal controls), it is essential to also consider the incorporation of a broader control, that is, a more comprehensive internal control that includes the analysis of municipal management.

Specifically in the municipalities, this need is relevant as long as they constitute the form of government closest to the population and satisfy the direct needs of the citizens. The current context of rapid change requires a vision of the future that determines explicit policies and formulations of appropriate strategies.

Specifically in the province of Misiones, being a young province, public entities in general as well as municipalities are still in a stage of institutional strengthening addressing different tools to improve their management.

It is perceived in the municipalities in general, and with greater emphasis in the smaller municipalities, a certain lack of definition and planning of objectives and goals, elaboration of strategies to achieve them, definition of criteria for the evaluation of results and measurement of the results obtained; which leads to some improvisation that can constitute a limitation to organizational growth.

From different organizations and proposals, training, strengthening programs and financial and technical support for the improvement of administrations are addressed.

Although progress has been made in different topics, in general they focus on aspects of legality control aimed at fulfilling the required accountability or management issues directly related to the execution of public policies, perceiving that there is still a gap in terms of internal control and the benefits it presents.

As discussed in the preceding paragraphs, internal control, included as a process within the organization's set of operations, would provide reasonable evidence regarding the achievement of the entity's objectives, measuring the effectiveness, efficiency, and economy of the processes. , as well as timely and reliable information, communication and regulatory compliance; acting as a preventive self-assessor.

For this reason, the present work hypothesizes that the correct implementation of internal control in small municipalities would contribute to an improvement in management, presenting benefits both for the organization and for the general public.

The objective of this work has been established to survey the current situation of internal control in the second-category municipalities of the province of Misiones, Argentina, in order to make proposals for good practices that allow an improvement in the internal control of small municipalities.

This work is of great interest to the municipal public sector since the implementation of good practices in terms of internal control would allow a more efficient and effective administration of municipal resources with the benefit that this entails for the general public.

DEVELOPING

Internal control and its importance in management

Internal control is defined as a comprehensive process applied by the highest authority, management and staff of each entity, which provides reasonable security for the achievement of institutional objectives and the protection of resources (Gamboa, Puente and Vera, 2016). . Internal control does not imply an end in itself, but it is one more means to achieve the objectives; Such is the case that an adequate internal control regime allows whoever is responsible for decision-making in organizations to have accurate, timely and reliable information on administrative management (Ivanega, 2016).

For Coopers & Lybrand (2007) internal control is a process, carried out by people (board of directors, management and other staff), in order to provide a reasonable degree of security regarding the achievement of objectives in a company. or more of the different categories: effectiveness and efficiency of operations (basic business objectives of performance and profitability, and safeguarding of resources), reliability of financial information (related to the preparation and publication of reliable financial statements and reports on them derived and published) and compliance with applicable laws and regulations (to which the entity is subject).

Quinaluisa Morán & others (2018) mention that internal control, like organizational structures, has evolved. Three generations are evident; the first, related to predominantly accounting and administrative controls, with little professionalization of those in charge of the internal control system. The second is characterized by a legal bias, with the incorporation of internal control structures and practices, and especially in the public sector, focused on the evaluation of internal control as a means to define the scope of audit tests, always seeking the compliance, and losing sight of quality. And the latest generation is focused on quality, being located at the high levels of the organizational structure in order to guarantee its efficiency.

In this sense, today internal control is seen as a facilitating tool for improving management, obtaining efficiency, economy, effectiveness and continuous improvement. Ultimately, the purpose is to check if the organization achieves its objectives.

From another perspective, internal control through its proactive action and taking into account that it is a preventive control, tends to eradicate or significantly reduce the risks to which the different types of organizations have been exposed, whether they are private or public entities. , for profit or not, large or small.

According to the COSO Report (2013), an international comprehensive control model, published by the Committee of Sponsoring Organizations of the Treadway Commission National on Fraudulent Financial Reporting, which provides a standard as a basis for identifying the best applicable practices, internal control consists of five components that are linked to each other and that generate a synergy forming an integrated system that responds to the changing circumstances of the environment. These components are: the environment or control environment, risk assessment, control activities, information and communication, and supervision.

In addition, four established categories of internal control objectives can be determined: objectives of a strategic nature, financial information, operations, and compliance with legal provisions and regulations.

Regarding the figures within the organization in charge of internal control, Abriani (2010) affirms that it is the absolute responsibility of the superior authority, the establishment of an adequate, efficient and effective internal control system.

However, this control must be integrated into the administrative processes, essential for the formation of the acts, without interfering in the actions of the entities. It is a chain of actions extended to all the activities inherent to the management and integrated to the other basic processes of the same; planning, execution and supervision. Such actions are incorporated into the structure of the entity and cover all members of the organization.

The management must set the objectives, the organization plan and delegate functions, responsibility and authority, since it is nourished by what is generated and produced by the intermediate and lower levels, these being the basis for decision making, information and results. facts that are generated in them.

And beyond the benefits that can be obtained, it is worth noting the relationship that must exist between the cost-benefit when determining the design and the depth of the controls to be carried out in each entity, depending on their exposure to risks.

Taking these premises into account, internal control, if it is applied in the appropriate manner, strongly contributes to obtaining optimal management, since it generates benefits for the entity's administration, at all levels, as well as in all processes, sub processes and activities.

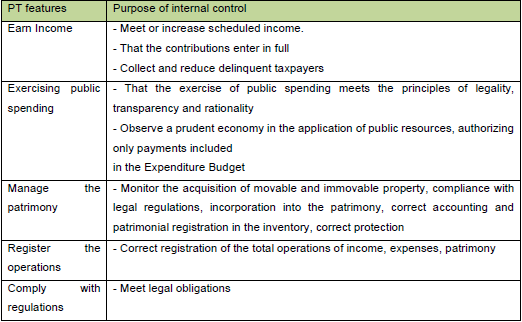

Good internal control practices in municipal entities

From the point of view of municipal entities, as public bodies, internal control should act as feedback for public policies. Municipalities today face increasingly broad decision-making fields, requiring an organizational structure in accordance with what is expected of them, which allows efficient and concerted decision-making, and which implies the greatest satisfaction of internal needs (of the institution) and external (from the community) with the best use of resources. Without leaving little room for the public manager to carry out the acts for which they were chosen by society, internal control must complement it to generate more efficient and productive management.

An adequate control practice will allow greater efficiency in the allocation of physical, human and financial resources, providing a basis of security and confidence in the performance of the officials involved (Castelli, 2010).

However, the governmental function of the municipalities should not be left aside, since they are not simply nuclei of administration, but rather they must solve problems that are political, of execution (Salinas, 2001); for which, internal control should focus on the appropriate management of the application of public resources to improve the well-being of the inhabitants of the place.

The current context of uncertainty and the demands in dynamic and complex environments, make it necessary for municipal entities, through the implementation of an internal control system according to their particular needs, the search for effectiveness, efficiency and economy; and the follow-up of a procedure called the three “D”:

- Capacity of the organization to identify new problems or challenges or the redefinition of the current ones, taking into account the changes in the environment and the expectations and needs of citizens (Diagnosis).

- Capacity of the organization to facilitate a process of formulation of policies, strategies and objectives necessary to face the new problems detected (Design).

- Capacity of the organization to deploy the strategies and objectives designed to implement the new solutions, overcoming conflicts and resistance and learning from their own experience (Development) (Parres García, 2010).

The internal control function in the public sector has as its fundamental purpose to act as a preventive evaluator, in the context of a proactive system, destined to the permanent verification of the adequate performance of public management.

In municipal entities, it may happen that the objectives and management plans are worked on empirically, without being defined in writing; which can generate unforeseen situations. If an adequate control environment and the corresponding risk assessment are installed, managing internal control in advance, this type of inconvenience can be prevented.

In this sense, and as a previous experience in the municipal field, it is worth mentioning the Superior Municipal Inspection Guide and its evaluation, of the State of Veracruz, Mexico, as a tool for putting effective control into practice and taking advantage of its functionalities, which provides control principles and guides for each sector of the municipalities.

It defines an internal comptroller, who is in charge of the implementation and start-up of the system, but also the head of each administrative unit is responsible for the appropriate institution of it; objectives and risk tolerance are defined; the implementation process of the internal control system in each dependency is detailed, based on feedback from the system itself and on the training of those responsible.

For training, conferences and teleconferences have been organized for heads of municipalities, those responsible for internal control and assistants. Access to a microsite has been provided on the website through which the processes that must be carried out to diagnose the existing internal controls and proceed to their improvement are disclosed.

As stated, this guide postulates the control process oriented to each dependency, considering that the result of internal control development and evaluation processes is greater when they are designed jointly with the administrative units, as detailed in the following frame:

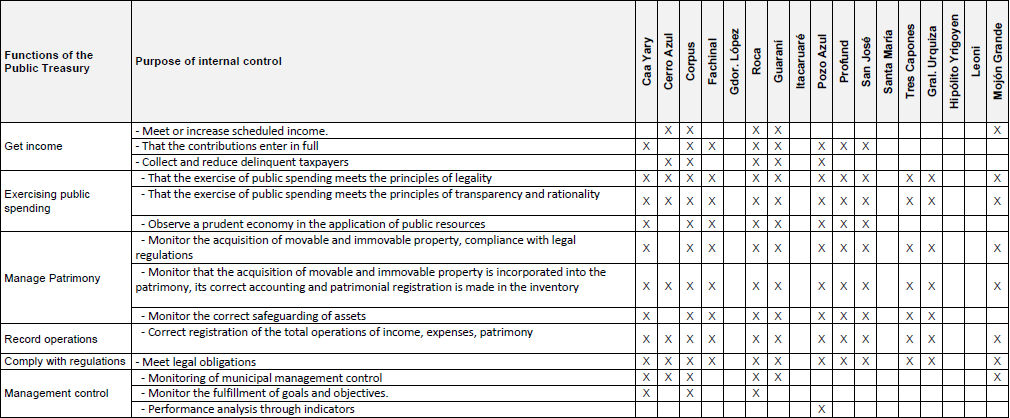

Table 1

Table of Purposes of Internal Control in relation to the functions of the Public Treasury (PT)

Note. Own elaboration based on Guide No. 5 of Municipal Internal Control and its Evaluation. http://orfis.gob.mx/guias2013/guia5.pdf accessed on 11/08/16. p.13 to 15

In this way, the importance of planning is visualized, of having defined its vision of the future and its mission. In this way, it is guaranteed to know the direction that the institution will follow (Luna de Giménez, 2001).

An adequate coherence must be kept between what is planned and what is executed, what is executed and what is controlled, and between what is controlled and evaluated. The assignment of responsibilities does not only imply the contrast with legal and accounting norms, but with objective performance guidelines (Groisman and Lerner, 2000). Even better if it is possible to segregate control by sector or by public finance functions.

To monitor compliance with results, internal control models are recorded that measure and evaluate everything produced externally (what service is provided and how satisfied the user is, in this case, the citizen), such as what is managed in inside organizations (with what resources is managed in relation to what is programmed and what type of processes are developed) (Sánchez, 2005).

The control system that is implemented, appropriate to the municipal structure itself, should be oriented towards achieving the best results for the administrator, for the user, for the citizen considered "client" in the metaphorical sense, which make it possible for the whole of the members of the municipality and its dependencies direct their efforts towards their satisfaction, at the same time that they develop a greater awareness of the cost in the use of the public resources used.

Survey of the internal control activities developed by the second category municipalities of the Province of Misiones

Methodology

In order to make an internal control proposal for municipalities, the control activities carried out by the second-category municipalities of the province of Misiones have been made known by conducting surveys via email, which were sent to municipal accountants.

In the province of Misiones there are a total of 51 second-category municipalities, having obtained a response from 17 of them, representing this amount 33.33%.

For the design of the submitted forms, the different control phases were considered in order to obtain field information linked to the control actions carried out in the municipal administration.

General questions related to internal control and its evaluation, action planning, and analysis of results were asked. Most of the questions that made up the survey allowed the selection of two options, providing in all cases the possibility of making clarifications or comments, that is, they were semi-structured. Only one of them was designed with a closed format, allowing only the selection of one option, if applicable.

Also, the purpose of internal control in relation to public finance functions was specifically analyzed, asking a set of questions with non-exclusive multiple response options, on the following topics: a) obtaining income; b) execution of political spending; c) asset management; d) registration of operations; e) regulatory compliance; and f) management control.

Based on the diagnosis of the situation of the municipalities under analysis, the internal control proposal for municipalities in general was raised.

Results obtained on internal control in general

In relation to internal control in general, municipal accountants have been consulted on aspects related to the theory and practice of internal control applied to municipalities, whether any municipal internal control procedure has been systematized and whether it contributes positively. to management improvement.

Thus, it has been inquired about the existence of some internal control guide and its evaluation and if the municipality effectively carries out an internal control that allows evaluations and comparisons of the results obtained with the programmed and budgeted, making possible the application of timely corrective measures before deviations detected. Likewise, it has been consulted on whether internal control actions are planned and if these are evaluated, and if they have carried out some type of control that allows to observe if the objectives and goals are met, preventing risks, detecting deviations and making corrections, which promotes efficiency, effectiveness, transparency and economy, safeguarding State resources and mitigating irregularities or acts of corruption. Finally, it was asked if they have received any training on quality management systems.

The result of the responses obtained in this regard is presented below:

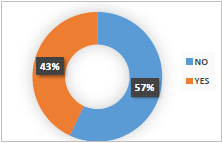

- In relation to whether there is an internal control guide and the evaluation of its use in the municipality.

In general, municipal accountants point out that municipalities do not have an internal control guide. Thus, 69% expressed themselves negatively and only 31% of them have indicated that they have this type of material. However, when observing what the indicated guide consists of, it can be verified that 40% of such answers referred to different provincial regulations as internal control guides, as well as the external control body linked to the executive and deliberative department. of the municipality itself. It is important to highlight that the type of regulation mentioned refers above all to aspects related to public accounting, not including the same issues of management or internal organization, but only issues related to legal aspects, responsibility and accountability, which They do not include internal control issues, aimed at management control for effectiveness and efficiency.

As more unique cases, there is a response that mentions as a guide Technical Resolution No. 7, a standard issued by the FACPCE and adopted by the CPCE of Misiones, but referring in particular to the external audit of financial statements; and the case of a municipality that points to a document provided by the Court of Accounts to the Mayor on the occasion of a training meeting in 2019 regarding issues to keep in mind at the time of change of managers.

The municipality of Hipólito Yrigoyen is noteworthy, which specified the methodology used by the commune regarding public works contracts and the collection procedure. He points out that, for contracting, every Monday jointly, the foreman, the municipal accountant and the mayor, plan what will be done in that area, observing the available funds and the work priorities, and carrying out at the end of the month, the Survey of the work in relation to what was planned and the costs applied, correcting deviations or errors to improve. As regards collection, every three or six months, a survey of pending tax collections is carried out to invite taxpayers to pay them, monitoring the invitations made, the responses by the taxpayer, and whether they were received. fees actually collected. It mentions these procedures, clarifying that other types of internal control are also carried out, even though there is no formally written instrument.

The graph of the responses to the question about whether there is an internal control guide and its evaluation is presented below:

Illustration 1

Internal control guide and its evaluation

Note. Own elaboration based on the surveys carried out

The graph reflects that the majority of those surveyed have answered that they do not have an internal control guide, nor the realization of it.

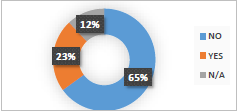

- In relation to whether the internal control carried out in the municipality allows evaluations and comparisons of the results obtained with the programmed and budgeted, allowing timely corrective measures to be taken in the event of detected deviations.

It is observed that, of the total number of municipal accountants who have responded to the survey, 12% have not expressed themselves in relation to the question in question.

On the other hand, to a greater extent they expressed themselves in the affirmative, stating in one case that such assessments depend to a large extent on the training of those responsible for the municipality. However, in a lower percentage they expressed that the municipality does not carry out internal control that allows evaluations and comparisons of the results obtained with what is programmed and budgeted, allowing timely corrective measures to be taken in the event of detected deviations.

Illustration 1

Internal control allows for evaluations and comparisons

Note. Own elaboration based on the surveys carried out

In relation to whether internal control actions are planned and then their results are evaluated.

Regarding planning, most municipal accountants have stated that internal control actions are not planned, however clarifying in some cases that, if they were to do so, it would be difficult to implement. A similar response has been obtained regarding evaluation actions, indicating in this case that such action is carried out informally.

Ilustration 2

Internal control planning actions

Note. Own elaboration based on the surveys carried out

llustration 3

Internal control evaluation actions

Note. Own elaboration based on the surveys carried out

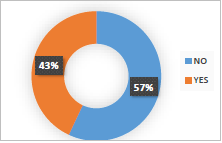

- On whether the municipality carries out a control that allows to observe if its objectives and goals have been met, preventing risks, detecting deviations that arise and making corrections, which promotes efficiency, effectiveness, transparency and economy, safeguarding state resources and mitigating irregularities or acts of corruption.

In this case, 53% of the answers were negative, while 47% answered in the affirmative, one of them highlighting that control fulfills above all the function of safeguarding state resources and reducing irregularities and/or acts of corruption.

Illustration 4

Control to verify compliance with objectives and goals

Note. Own elaboration based on the surveys carried out

In relation to whether they have received any training in quality management systems.

100% of those surveyed stated that they had not received any type of training in quality management systems. Only the municipality of Caa Yary indicated that during 2019 it attended a training given by the TC.

Results obtained on the purpose of internal control in the functions of the PT

Taking into account the objectives and goals of public finance and the municipal internal control guide and its evaluation by the Veracruz State Supervisory Body (2013), a series of specific aspects related to the purposes of internal control in each of the functions of the municipalities.

Thus, municipal accountants have been asked to indicate whether the internal control carried out in their municipalities meets certain purposes, being able to select all the options they consider correct, within each of the functions detailed below: a ) earning; b) execution of political spending; c) asset management; d) registration of operations; e) regulatory compliance; and f) management control.

The table with the details of the responses obtained is added as an attached table. It should be clarified that the data presented below reflect, within a grid of internal control purposes indicated for each public treasury function, the percentage that has been obtained based on the responses of municipal accountants.

From the analysis of the collected data, it is observed that, in relation to obtaining income, 29% of those surveyed have stated that the purpose of internal control is to meet or increase programmed income and collect or reduce delinquent taxpayers. 47% of them have indicated that what is intended is that the contributions be paid in full.

In relation to public spending, 71% of municipal accountants indicated that the purpose of internal control is that its exercise meets the principles of legality, transparency and rationality. Furthermore, 47% indicated that internal control seeks to observe a prudent economy in the application of public resources.

Regarding the administration of assets, 65% of those surveyed indicated that internal control seeks to monitor compliance with legal regulations at the time of the acquisition of movable and immovable property, 71% indicated that it verifies that these acquisitions are incorporated into the patrimony and that its correct accounting and patrimonial registration is carried out in the inventory, and 59% indicated that internal control would fulfill the purpose of monitoring the correct safeguarding of patrimony.

Regarding the registration of operations, 71% indicated that internal control has the purpose of analyzing the correct total registration of income, expenditure and equity operations.

Likewise, 71% indicated that internal control attends to compliance with legal obligations.

And finally, in relation to management control, 35% indicated that the purpose of internal control in this area pursues the monitoring activities of this type of control; 18% monitoring compliance with goals and objectives and only 6% indicated that it is used for performance analysis through indicators.

It is important to note that three of the seventeen municipalities surveyed, three of them have not responded to any of the options presented in this question, having expressed their opinions in previous questions.

Analysis of internal control in the second category municipalities of Misiones

Based on the survey of the data carried out and the analysis of the answers obtained, some conclusions can be reached in relation to the internal control of the second-category municipalities of the province of Misiones.

Thus, it can be pointed out according to what was mentioned by the municipal accountants, that there is, in general, a certain lack of knowledge on the part of municipal officials regarding the objectives pursued by internal control, evidenced by the inconsistency in some responses. It can be mentioned as an example that in several cases it was indicated in the affirmative with respect to whether the internal control carried out by the municipality allows evaluations and comparisons of the results obtained with what was programmed or budgeted, as well as the corrective measures to correspond, however, On the other hand, they responded that planning and evaluation actions related to the issue at hand are not carried out.

Likewise, there is a low knowledge of the regulations and concepts related to internal control, such as the COSO report, confusing the objective pursued by this type of control, with the legality control required by the regulations applicable to the public sector.

On the other hand, a certain informal nature of the evaluation actions carried out by the municipalities in this matter is perceived, an issue that may be linked to the lack of clarity of the objective and concepts related to internal control, raised in the previous paragraph. For example, in the query in relation to whether the internal control carried out in the municipality allows evaluations and comparisons of the results obtained with the programmed and budgeted, allowing timely corrective measures to be taken in the face of detected deviations, it is observed that, of the total number of Of the municipal accountants who have responded to the survey, 12% have not expressed themselves in relation to the question in question. It can be estimated that the complexity in the degree of detail of the internal control that the question reflects has not allowed them to determine an answer, when even it only included the possibility of answering yes or no. Another way of interpreting this lack of response is that it is likely that this type of control is not carried out in these communes. Likewise, in the case of the query on training received related to internal control, only one answer was affirmative. However, from the clarification of the aforementioned, it appears that the training carried out by the Court of Auditors was referred to the act of change of managers and not to the subject matter consulted, from which some confusion of the concepts and objectives of internal control can be deduced.

Possibilities for improvements in internal control for municipalities

Reality shows that it is common to find municipalities with little infrastructure, as well as few institutional capacities, raising the question: Is there any possibility that municipal administrations can improve their management?, which leads us to ask ourselves: is it necessary to improve control internal and how? Perhaps what is pertinent to review is what needs to be improved in terms of internal control by working on what. However, all the deficiencies exposed in previous paragraphs are actually areas of opportunity, since internal control has tools and mechanisms that can directly affect the effectiveness and efficiency for the development of better municipal public management.

It should be noted that, although the framework of the COSO report has been adopted as regulatory support, relevant content is provided to understand the main directives in the implementation, management and control of an internal control system, considering the characteristics of the municipalities according to to the study carried out on the second category of the province of Misiones. Thus, from this particular vision, the possibilities of improvements in terms of internal control for these public entities are framed, taking into account the knowledge obtained from the surveys carried out and the application of the same to their daily reality.

This is how internal control, a process executed by the staff of each community entity, is essential for officials, since it allows them to detect operational and functional deviations in the implementation of political or administrative decision-making, and a reliable, valid and effective tool. to determine the improvements or changes that must be produced to meet the specific objectives of each government administration.

This conceptual framework allows us to identify possibilities for improvement from the perspective of the internal control components, which are linked and serve as a guideline to determine when the system is reasonable. Among them, stand out:

- Control environment: promote training activities promoting a culture of staff commitment, whose general objective is to monitor the proper functioning of the internal control system and its continuous improvement, aspects that, in addition to tending to monitor the achievement of objectives. support the transparency of management. The training of public agents is a demonstration of internal control that can considerably reduce errors, since by understanding the administrative processes and procedures and updating them with new ones, deviations in their application are less likely to arise. Communal administrations can adopt measures to expand the coverage and depth of training functions in matters of control and public ethics, taking into account that one of the main challenges detected, according to the responses to the questionnaire, to integrate the components and internal control processes with the administration of daily activities in public institutions of second category municipalities, is the existence of personnel with insufficient skills and knowledge about internal control, standards and tools.

Competent and reliable personnel are necessary for effective control, therefore the methods of recruitment, guidance, training, promotion and remuneration are an important part of the internal control environment. The actions to be implemented, among others, for this component of control in municipal offices are: define the organization chart of the municipal administration, so that everyone knows the hierarchical structure and the people who occupy each position, keeping it updated and clearly defining the levels of responsibilities; establish within the organization manuals, processes and procedures, for example, the methodology, regulations and responsibilities in the management of permanent funds and petty cash; the legal provisions governing cost containment; determination and authorizations for the granting of per diems. In order to have effective controls, each municipality must have objectives that are supported in its annual budget.

- Regarding risk assessment, each municipal management faces a variety of risks, so mechanisms are needed to identify and evaluate them. These may involve, for example: bad decisions due to the use of erroneous, incomplete or inappropriate information; accounting records that do not reflect the municipal economic and financial reality, or that do not include all assets or liabilities, or records of commitments and imputations that do not reflect the integrity of the transactions carried out by the municipality in its different budget stages; negligence in the protection of assets; acquisition of goods based on uneconomic practices that include poor quality due to not conforming to the samples, overpricing, as well as manifest attitudes of non-compliance with laws and regulations in the public procurement and contracting regime, in addition to the possibility of the emergence of risks caused by fraud or for large, complex and unusual transactions. As a starting point, simplifying the procedures and times of internal reports required by municipal administrations is essential to improve this last type of risk.

- The selection and development of control activities through technologies is a great contribution to control mechanisms. The focused use of technology allows preparing and processing a large amount of data from records, databases and information systems, which can be used to generate knowledge about management, that is, the possibilities of designing tools based on technologies are opened. for citizen control, which allow access to timely information on public resources and their spending at various levels of disaggregation, and therefore, the involvement in public control to generate cross-references of information on the municipal budget, purchases of goods and contracts of works, which cannot be carried out manually due to its volume.

Among the opportunities, the practice of selective reviews stands out; focusing on the provision of municipal services, verifying the conformity and satisfaction of the users; the implementation of new modes of organization and relationship with the citizenry. Although the benefit of having an internal control system, among others, is the reasonable security of achieving greater efficiency, effectiveness and transparency in operations, it being necessary for municipal governments to make public information available to the public, it is also essential, from the scope of internal control, to know to what extent the beneficiaries and users are satisfied with the procedure or service received by the municipal administration, therefore, the quality of care, the evaluation of the provision of public services, which through citizen participation can carry out the management or the opinion that citizens expose through complaints, suggestions or claims. In this way, this information makes it possible to reduce the risks of fraud, to know the citizen's assessment of the service received and to determine what are the opportunities for improvement in management.

In turn, through the actions carried out by governments, there are effects on the citizens that it reaches and for this reason it is opportune to include indicators that evaluate the fulfillment of the different objectives embodied in the government plan, but from the perspective of the beneficiary. , that is, through the degree of user satisfaction.

When evaluating the effectiveness of the provision of services, the degree to which the municipal entity, in relation to the budgeted figures, managed to meet the objectives and goals established in its government plan, measured in terms of quantities of services/products provided, is being analyzed. compared to the resources estimated in the calculation of annual resources and effectively committed in budget execution.

For the purpose of evaluating it, for example in the strengthening of primary health care, the physical infrastructure of municipal centers, dental medical equipment, medical supplies, vaccinations, constitute essential elements to analyze the health service provided: nursing and medical, applied vaccines, medical and laboratory services, dental consultations that the population received in favor of prevention and health promotion, allowing to determine and analyze the increase or decrease in benefits on a monthly, quarterly or with respect to previous efforts.

The control activities component occurs at all levels and functions and includes, for example, activities such as: spending authorizations, contract approvals, verifications in the movement of funds, separation of functions and responsibilities, safekeeping and protection of assets, among other. In any possibility of improving internal control in municipalities, certain actions can be indicated, such as: implementing controls for the appropriate use of official vehicles, fuel and maintenance; periodically update passwords or access codes to systems or computer programs used by municipal agents; establish the type of access and restrictions to computer systems and equipment for each of the users according to their profile; perform periodic backups of relevant information from municipal computer equipment; implement a control of consumer goods (spare parts, inputs, office supplies, etc.) in the place determined by the communal administration; carry out periodic counts of petty cash and permanent funds, as well as the rendering of advance funds; monitor the requests made by taxpayers and citizens in order to measure the impact on the attention to them.

- On the other hand, the development of information and communication systems allow the strengthening of community management, since they enable the flow of information (budgetary, accounting, financial, operational, administrative) through all the areas that need it, expedite statistical analysis allowing the preparation of multiple types of reports useful for management, simplify the execution of administrative processes, improve user service, allow the implementation of electronic records, among others.

Implement an electronic platform of internal and external general information (web page, social networks, others), in which the different events, legal provisions, expiration and payment schedules, policies, plans, statistics and results of the actions and municipal benefits, is one of the factors that allows optimization of internal control, as well as rendering accounts to all the inhabitants of the city on the actions and performance of the municipal administration, through the portal of access to information (also identified as portal of transparency, mandatory for municipalities adhering to the fiscal consensus, which establishes the distribution of nation-province-municipal resources).

- Finally, both individual controls and the internal control system as a whole must be frequently supervised and monitored, since effective internal control can lead to improved performance of municipal administrations by allowing them to timely identify and correct internal control problems and produce reliable information for decision-making by administrators, in short, improve their effectiveness and efficiency.

CONCLUSIONS

An analysis of the current situation of internal control activities in second-category municipalities in the province of Misiones has been carried out, based on the evidence of the importance that a correct implementation of this type of control has in the claim of efficient, effective and transparent municipal management.

In compliance with the objective, the methodology applied has been to carry out surveys of municipal officials in charge of control, according to current regulations, understanding as such municipal accountants. The approach to the surveys is based on the functions of the public treasury, namely: obtaining income, execution of public spending, administration of assets, registration of operations, compliance with regulations and management control.

The results obtained have shown a certain degree of ignorance of internal control standards, such as the COSO Report, with its consequent effect on the lack of adequate implementation, absence of planning and measurement of the results obtained. The answers revealed the absence of internal control guides, which stipulate in a written document the purposes of control, the necessary feedback and the training of the participants.

Based on the research carried out, it is interpreted that the controls implemented in these organizations fundamentally pursue compliance with regulations and legal provisions, oriented towards accountability to the external control body, the perception of resources and the prevention of corruption.

Notwithstanding, and without neglecting the cost-benefit relationship that any control system must have, taking into account the size of small municipalities; the hypothesis raised at the beginning of the work is verified, while this correctly implemented control would promote an improvement in management, focusing on results, emphasizing the achievement of objectives (previously defined) with effectiveness, efficiency, reasonableness and economy, in the implementation implementation of strategies to achieve them and in the evaluation of results after a period, through a specific method (also previously defined), which could be specified as performance indicators. The fact of having an effective internal control system implies a certain potential to detect risks to which the municipality is exposed as an organization and to correct deviations from the objectives set in time, as long as this control is carried out ex ante, concomitant and subsequent

The improvement in management for the organization itself implies the use of internal control as a tool for institutional strengthening and increasing the level of security regarding the achievement of objectives, through the provision of reliable information for decision-making, evaluating the quality in the activities carried out for the fulfillment of goals, accompanying the progress of the management, as an articulated instrument, contributing to the planning, execution and supervision processes of the municipality, with self-control and self-evaluation dynamics.

The fact that internal control focuses on results, on the achievement of objectives with effectiveness, efficiency, reasonableness and economy would contribute directly to an improvement in the municipal administration, and indirectly, through a positive impact on the citizenship in general, since it would enable transparency in management, in the objectives set and the way to carry them out, generating trust and reinforcing governability.

REFERENCES

Please refer to articles in Spanish Bibliography.

BIBLIOGRAPHICAL ABSTRACT

Please refer to articles Spanish Biographical abstract.

ANEXO - Propósitos del control interno en las funciones de la hacienda pública municipal